The deployment of technological innovations to enhance efficiency and accuracy has led to a considerable impact on various commercial sectors globally. In the absence of relevant technological innovations, it would have been burdensome to capture, let alone store and process voluminous commercial transactions. The present paper aims to expounding the significance of electronic device machines (EDMs) as a technological innovation in the management of taxes. A review methodology was utilized to analyze extant literature with regards to the topic. A predetermined inclusion and exclusion criteria was employed to determine the relevance of papers that were analyzed. Through thorough synthesis of articles that were analyzed, the study found four benefits of EDMs as a technological innovation in the management of taxes. Firstly, EDMs prevent tax data manipulation which is rampant when taxes are collected manually; secondly, EDMs allow for real-time transactions where tax data is instantly sent to tax collecting bodies thereby improving efficiency; thirdly, EDMs prevent tax evasion thereby enhancing revenue collection; and finally, EDMs provide tax audit trail from the data sources thereby enhancing tax compliance. In a nutshell, adoption of EDMs as a technological innovation is vital in the process of managing tax as it minimizes challenges faced by tax collecting bodies when the exercise is done manually.

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited.

Taxes play a pivotal role as an enabler for governments in the management of macroeconomic conditions. Precisely, taxes form the principal source of income toward the budget of a nation, promote investments, avert possible inflation, preserve regional industries, and promote equitable distribution of income throughout the society thereby reducing wealth inequalities

[11]

Le, T. N. T. Hai, Y. M. T. Thi, T. C. & Hong, M. N. T. (2024). The Impact of Tax Awareness on Tax Compliance: Evidence from Vietnam. Journal of Tax Reform, 10(2), 214-227.

[11]

. As such, the need to properly manage taxes cannot be overemphasized because failure to do so can lead to devastating effects to economic outturn of nations. Some critical issues that entail effective tax management border on the development, implementation and review of tax policies, sensitizing the citizenry on the available policies, enhancement of compliance while at the same time, reduce cases of evasions

[11]

Le, T. N. T. Hai, Y. M. T. Thi, T. C. & Hong, M. N. T. (2024). The Impact of Tax Awareness on Tax Compliance: Evidence from Vietnam. Journal of Tax Reform, 10(2), 214-227.

[11]

.

Researchers have proved that technological innovation is now the main driver of economic growth in the pursuit of value creation

[13]

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

[13]

. To this effect, the emergence of various technological innovations has provided new ways of doing things thereby enhancing both efficiency and effectiveness. One of the financial sectors that has lately witnessed the influx of digitalization is that of taxation which is the mandatory fee imposed on individuals, and institutions by the government via tax administration

[3]

Aduamoah, M. Yinghua, S. & Anomah, S. (2017). Applicability of Computerised Accounting System in Improving Financial Accuracy in Ghana SMEs. Innovation and Management.

[13]

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

[3, 13]

. To that end, technological innovation is essential in taxation, particularly when it comes to computerizing corporate procedures and systems. As taxpayers' businesses grow more complex, the need to have a tailor-made system that will be able to capture the transactions with efficiency cannot be overemphasized.

Getting the right taxes paid on time without compromising taxpayer confidence in tax administration is the main goal of tax administration

[13]

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

[13]

. As such, there is friction between tax administration and taxpayers regarding tax evasion, non-registration, and non-submission of tax returns

[13]

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

[13]

. Extensive research has been done on the reasons why taxpayers fail to honour the accurate sum of levies

[13]

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

[13]

. The results have shown that tax systems are complex and unfair, revenue information services are inadequate, taxpayers lack self-assurance in the tax administration, the likelihood of being caught evading is high, and that the benefits of evading outweigh the penalties. These elements have an impact on taxpayer compliance, which leads to a tax gap emanating from the actual taxes paid against those that were supposed to be paid

[13]

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

[13]

. According to the authors, one of the techniques to gauge compliance is to measure the tax gap. In other words, in order to comply with tax laws, taxpayers must disclose to tax authorities the true tax base; calculate the tax liability accurately; timely compile the tax return; and pay the required amounts according to the guiding schedule. Since all these stem from reliable data reporting, tax administrators developed the technological innovation of electronic fiscal devices (EFDs) that responds to the status quo.

2. Literature Review

Tax administrations across the globe have digitized their systems and operations through advances in technology to increase efficiency and attain high compliance levels

[4]

Ajayi, E. O. & Yidiat, O. (2021). Impact of e-tax filing on tax revenue generation in Nigeria. Global Journal of Accounting, 7(1), 25-36.

[4]

. According to the authors, technical improvements that have been embraced include electronic fund transfers, telephone payments, e-commerce, and electronic tax return submission. Through the adoption of such technological advances, the traditional way of managing taxes is slowly being phased out and technology is taking center stage. This notion is in line with the Theory of Reasoned Action (TRA) which asserts that people tend to employ technological innovations if they are convinced beyond reasonable doubt that its benefits outweigh the traditional way of doing things

[21]

Venkatesh, V. Morris, M. G. Davis, G. B. & Davis, F. D. (2003). User acceptance of information technology: Toward a unified view. MIS quarterly, 425-478.

[21]

. This, in other words, means that people have the behavior of transitioning from the traditional way of conducting business to a modern way when benefits of the latter outweigh the former. The TRA feeds into the Technology Acceptance Model (TAM) which asserts that when users are convinced that the current innovation has capability of enhancing efficiency and effectiveness, they accept it easily as a solution moving forward

[22]

Wu, J. H., & Wang, S. C. (2003). An empirical study of consumers adopting mobile commerce in taiwan: analyzed by structural equation modeling. PACIS 2003 Proceedings, 6.

[22]

.

EFDs are devices that are put at taxpayer business locations and are internet connected to a tax administration server

[13]

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

[13]

. The process used to compute, collect, and administer taxes in electronic medium is known as electronic taxation. E-taxation entails a system where tax returns are filed electronically, typically eliminating the need to file any paper returns

[7]

Awai, E. S. & Oboh, T. (2020). Ease of paying taxes: The electronic tax system in Nigeria. Accounting and taxation review, 4(1), 63-73.

[7]

. It involves making use of software, the internet, and internet technology for a range of tax administration and enforcement functions. Globally, EFDs have been put into practice and they are designed to store real-time data on taxpayer business transactions and reports are sent to the tax authority by it

[4]

Ajayi, E. O. & Yidiat, O. (2021). Impact of e-tax filing on tax revenue generation in Nigeria. Global Journal of Accounting, 7(1), 25-36.

[13]

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

[4, 13]

. EFDs are designed in such a way that they are capable of recording sales in order to secure tax data for auditing needs and control data to remove risks associated with declaration such as failure to report or reporting figures that are lower than the actuals

[13]

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

[13]

.

Scholars assert that e-taxation is a computerized means of progressively wiping out traditional administration of taxes across the globe

[20]

Umenweke, M. N. &Ifediora, E. S. (2016). The law and practice of electronic taxation in Nigeria: The gains and challenges. NAUJILI. 101-112.

[20]

. It is accomplished when taxpayers honour their dues electronically from their bases like workplaces, and elsewhere as long as they are able to connect to the internet. Through this way, tax administrators are able to track defaulters and go after them on the web portal via the electronic tax history of the tax payer. The EFD has proven to be a pivotal instrument in combating bottlenecks of any tax system as it is capable of providing the much needed support, education, and information necessary for the taxpayer which in turn, facilitates compliance and administration. In the same vein, EFD guarantees a reduced cost of administering taxes thereby enhancing efficiency

[1]

Abah, J. (2015). Technological innovation and banking in Ghana: An evaluation of customers' perspective. American Academy of Financial Management, 1(3), 338-356.

[1]

. Several studies have been conducted which have confirmed the positive impact of EFDs towards effective management of taxes across the globe

[4]

Ajayi, E. O. & Yidiat, O. (2021). Impact of e-tax filing on tax revenue generation in Nigeria. Global Journal of Accounting, 7(1), 25-36.

[7]

Awai, E. S. & Oboh, T. (2020). Ease of paying taxes: The electronic tax system in Nigeria. Accounting and taxation review, 4(1), 63-73.

[12]

Martin, L. O. Obongo, B. M., Magutu, P. O. and Onsongo, C. O (2010). The Effectiveness of Electronic Tax Registers in Processing of Value Added Tax Returns, African [J]. Journal of Business and Management, (1): 44-55.

[13]

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

[4, 7, 12, 13]

.

Despite availability of studies bordering on technological innovations with regard to management of taxation, literature is still devoid of studies that specifically consolidates the benefits of EFDs in the management of taxation. The available benefits are fragmented in various studies thereby making it difficult to follow them through. The present study, therefore, aims to bridge that gap.

3. Methodology

Key literature review methodologies, including narrative reviews, mapping reviews, descriptive reviews, theoretical reviews, umbrella reviews, meta-analyses, and systematic reviews are highlighted authors as being available to researchers

[16]

Paré, G. Trudel, M. C. Jaana, M. & Kitsiou, S. (2015). Synthesizing information systems knowledge: A typology of literature reviews. Information & management, 52(2), 183-199.

[16]

. Nevertheless, despite the abundance of review options, selecting the best one depends on the goals of the study and the nature of the problem being investigated

[17]

Popay, J. Roberts, H. Sowden, A. Petticrew, M. Arai, L. Rodgers, M. & Duffy, S. (2006). Guidance on the conduct of narrative synthesis in systematic reviews. A product from the ESRC methods programme Version, 1(1), b92.

[17]

. In order to achieve the goal of bringing together the benefits of EFDs in the management of taxes drawn from different authors, the current study adopted the narrative review. Though adoption of this approach, the study objective was effectively accomplished.

To reduce potential bias that could emanate from the retrieval and selection of the papers, the pre-determined search guidelines were shared among the three authors and each one conducted the search at their own time. At the end, the results were compared and where there were discrepancies, consensus by at least two of the three authors was being sought. Based on the available guidelines, the following standards were applied in order to preserve objectivity when sourcing the study materials

[18]

Rosenbusch, N. Rauch, A. & Bausch, A. (2013). The mediating role of entrepreneurial orientation in the task environment–performance relationship: A meta-analysis. Journal of management, 39(3), 633-659.

[18]

. First, the primary journal database, Scopus, was searched using key terms. Other journal databases such as Elsevier, Taylor & Francis, Sage, Emerald, and Inderscience were added on the list

[9]

Flick, U. (2015). Introducing research methodology: A beginner's guide to doing a research project. Sage.

[15]

Panneerselvam, R. (2014). Research methodology. PHI Learning Pvt. Ltd.

[9, 15]

. According to proposition made by scholars, the primary goal of this search was to delve deeper into relevant study materials about the use of digital devices in the management of taxes in various economies across the globe

[5]

Almuraqab, N. A. S. & Jasimuddin, S. M. (2017). Factors that Influence End?Users’ Adoption of Smart Government Services in the UAE: A Conceptual Framework. Electronic Journal of Information Systems Evaluation, 20(1), 11-23.

[5]

.

Additionally, a manual search was conducted through the majority of relevant journals like the following: Global Journal of Accounting, Journal of Tax Reform, Information & Management, Accounting and taxation review. Finally, to make sure that further studies pertinent to the study issue have been taken into account, the reference sections of the selected study materials were also perused and some articles were picked from there.

During the process of looking for the study materials, four key terms were employed to stay focused on the study area: “Electronic fiscal device”, “tax compliance”, “tax management”, and “taxation”. Upon accessing the paper, a quick perusal of the abstract was being conducted to get a general idea of the work and assess its relevance to the subject at hand before taking it on board. Timeframe for the papers was left open to ensure accessibility of adequate papers based on the fact that the search for papers was limited to the pre-determined key words.

After the study materials were obtained over the internet, they underwent an additional manual screening procedure by the authors. The exclusion criteria that was employed led to removal of book chapters, duplicates, and non-English papers. The inclusion criteria were based on articles that are in English, not book chapters, and from credible databases. A total of 30 papers were initially retrieved from various sources but after screening, 16 papers were found to be directly linked to the objective of the study. These studies were then categorized into associated sub-themes according to then benefits identified.

4. Key Findings

Globally, EFDs have been put into practice and they have proved to positively impact tax administrations

[2]

Adegbie, F. F. Enerson, J. & Olaoye, S. A. (2022). An empirical investigation into the relationship between electronic tax management system and tax revenue collection efficiency in selected states in South West, Nigeria. International Journal of Accounting Research, 7(1), 43-53.

[7]

Awai, E. S. & Oboh, T. (2020). Ease of paying taxes: The electronic tax system in Nigeria. Accounting and taxation review, 4(1), 63-73.

[14]

Olaoye, C. O. & Atilola, O. O. (2018). Effect of e-tax payment on revenue generation in Nigeria. Journal of Accounting, Business and Finance Research, 4(2), 56-65.

[2, 7, 14]

. Entries 4.1 through 4.4 consolidate the key benefits of adopting EFDs in managing taxes based on the synthesis of the retrieved literature.

4.1. Prevention of tax Data Manipulation by Tax Payers

It should be emphasized that not all tax payers are willing to honour their tax obligations because it is in the best interest of most income earners to maximize their disposable income

[19]

Srinivasan T. N. (1973). Tax evasion: A model. Journal of Public Economics, 2(4): 339–346.

[19]

. According to the author, taxpayers are consistently devising strategies to reduce the amount of tax which they have to pay. Among other things, one of the ways which taxpayers can use to evade tax is through manipulation of tax figures so that they can pay less than the actual amount

[6]

Allingham, M. & Sandmo, A. (2002). Income tax evasion: A theoretical analysis. Taxation: Critical Perspectives on the World Economy, 3, 305-318.

[6]

. It should be emphasized that not all tax payers can manipulate tax figures. However, it should also be indicated that there are some potential taxpayers who indulge themselves in various malpractices aimed at avoiding tax obligations

[6]

Allingham, M. & Sandmo, A. (2002). Income tax evasion: A theoretical analysis. Taxation: Critical Perspectives on the World Economy, 3, 305-318.

[6]

. Against this background, introduction of EFDs prevents manipulation of tax data as it replaces manual transactions

[2]

Adegbie, F. F. Enerson, J. & Olaoye, S. A. (2022). An empirical investigation into the relationship between electronic tax management system and tax revenue collection efficiency in selected states in South West, Nigeria. International Journal of Accounting Research, 7(1), 43-53.

[2]

. This maximizes tax collection and is also an encouragement to other tax payers who honour their tax obligations.

4.2. Allow for Real-Time Transactions

Challenges with compliance include, but are not limited to, failure to register, failure to submit the required returns, tax fraud as well as evasion

[4]

Ajayi, E. O. & Yidiat, O. (2021). Impact of e-tax filing on tax revenue generation in Nigeria. Global Journal of Accounting, 7(1), 25-36.

[7]

Awai, E. S. & Oboh, T. (2020). Ease of paying taxes: The electronic tax system in Nigeria. Accounting and taxation review, 4(1), 63-73.

[12]

Martin, L. O. Obongo, B. M., Magutu, P. O. and Onsongo, C. O (2010). The Effectiveness of Electronic Tax Registers in Processing of Value Added Tax Returns, African [J]. Journal of Business and Management, (1): 44-55.

[13]

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

[14]

Olaoye, C. O. & Atilola, O. O. (2018). Effect of e-tax payment on revenue generation in Nigeria. Journal of Accounting, Business and Finance Research, 4(2), 56-65.

[4, 7, 12-14]

. According to the authors, these malpractices pose a risk to the collection of income. The introduction of EFDs, therefore, aids in capturing and recording of business transactions, including sales, as they happen thereby preventing risks associated with having backlogs. These devices provide tax authorities with access to taxpayer data since they are interlinked through the use of internet to the servers of tax administrators. The goal is to obtain timely and reliable information.

4.3. Mitigation of Tax Evasion

Tax evasion is another malpractice portrayed by some tax payers

[7]

Awai, E. S. & Oboh, T. (2020). Ease of paying taxes: The electronic tax system in Nigeria. Accounting and taxation review, 4(1), 63-73.

. In a study that involved a cross-section of taxpayers, some of whom used EFDs and others who did not, it was found that there was a rise in VAT generation and a reduction in non-compliance on the part of the EFD users compared to the control group

[7]

Awai, E. S. & Oboh, T. (2020). Ease of paying taxes: The electronic tax system in Nigeria. Accounting and taxation review, 4(1), 63-73.

[7]

. Various compliance metrics were requested, such as the rate of return submission, ratio between VAT to GDP, rate of compilation, and quantity of devices to VAT generated

[11]

Le, T. N. T. Hai, Y. M. T. Thi, T. C. & Hong, M. N. T. (2024). The Impact of Tax Awareness on Tax Compliance: Evidence from Vietnam. Journal of Tax Reform, 10(2), 214-227.

[11]

. This means that there are several ways that constitute tax non-compliance. Introduction of EFDs, therefore, mitigate such evasion malpractices.

4.4. Provision of Tax Audit Trail from the Data Sources

An audit trail is a computerized track that documents a transaction's history from the beginning to the end of its processing inside a business

[3]

Aduamoah, M. Yinghua, S. & Anomah, S. (2017). Applicability of Computerised Accounting System in Improving Financial Accuracy in Ghana SMEs. Innovation and Management.

[13]

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

[3, 13]

. According to the authors, an auditor may track financial transactions from the general ledger to the source document and observe the complete transaction process through the audit tracking element, which is included as a component within the EFD system. Though the provision of the audit trail module, there is no way a tax payer can hide business transactions since the EFD is in a position of capturing and storing all transactions that pass though it.

5. Discussion

Every nation requires resources in order to provide for its population. One frequent method of generating these resources is through taxes

[10]

Islahı, A. (2015). Ibn Khaldun’s theory of taxation and its relevance. Turkish Journal of Islamic Economics, 2(2), 1-19.

[10]

. The author claims that governments utilize the money they get from their constituents to pay for necessities like goods and services. This implies that in order for governments to function properly, they need funding. Part of that funding is generated from taxes paid by the citizenry and corporations. The way governments operate is by collecting taxes and redistributing them to the populace through a variety of social and economic responsibilities.

Researchers have highlighted a number of challenges associated with tax management especially bordering on compliance

[23]

Xu, Y. (2010). Reforming value added tax in mainland China: a comparison with the EU. Revenue Law Journal, 20(1).

[23]

. According to the author, much as tax collectors would like to maximize collection of revenue, some tax payers engage themselves in malpractices like evasion and fraud. It is against this background that tax administrators have been coming up with various strategies aimed at enhancing tax collection as well as mitigating the tax related malpractices

[23]

Xu, Y. (2010). Reforming value added tax in mainland China: a comparison with the EU. Revenue Law Journal, 20(1).

[23]

. One of such strategies is the utilization of technological advancements in managing the taxes, particularly the EFDs

[13]

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

[13]

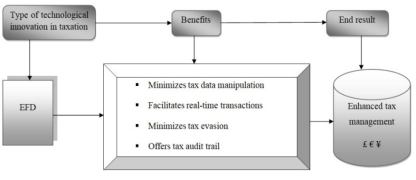

. According to the authors, EFDs have proven to be essential innovations in mitigation of compliance risks associated with taxation. Precisely, compliance has so far been enhanced in taxation through the adoption of EFDs. Figure 1 is therefore a framework that consolidates the benefits of EFDs in the management of taxes based on the findings from the analyzed articles. By bringing together the benefits in a single framework, the essence of EFDs is enhanced thereby encouraging tax administrators to adopt this technological innovation.

Figure 1. Benefits of EFD as a technological innovation in the management of taxes.

From Figure 1, it can be established that the benefits that emanate from utilization of EFDs in managing taxes are leading to enhanced management of the taxes. Precisely, through acceptance and utilization of EFDs, four key benefits are realized: minimization of tax data manipulation, facilitation of real-time transactions, minimization of tax evasion, and availability of tax audit trail. These benefits, put together, lead to enhancement of tax management.

Figure 1 further means that ignoring the EFD as a technological innovation in managing taxes will eventually adversely affect the management of taxes. Precisely, in the absence of the EFDs, the manipulation of tax data will prevail, transactions will be manual, evasion will be rampant and there will be no audit trail. These will in turn negatively impact the tax management. Table 1 further depicts the benefits, and associated sources.

Table 1. Benefits of EFD as a technological innovation in the management of taxes, sources inclusive.

S/N

Key benefits established

Sources

1

Minimizes tax data manipulation

[2]

Adegbie, F. F. Enerson, J. & Olaoye, S. A. (2022). An empirical investigation into the relationship between electronic tax management system and tax revenue collection efficiency in selected states in South West, Nigeria. International Journal of Accounting Research, 7(1), 43-53.

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

The present study posits both practical and theoretical connotations. Practically, it offers insights to various economies on how EFDs are beneficial in as far as efficient and effective management of taxes is concerned. By highlighting the benefits, the study acts as an inducement to policy makers to make informed decisions towards adoption of EFDs in managing taxes, Further, the benefits are not only accrued to tax administrators but also the tax payers since they are able to find the necessary tax information at their fingertips. The benefits are therefore relevant to both parties (i.e. the tax collector, and the tax payer).

Theoretically, the paper adds value to the already published studies regarding proper management of taxes through adoption of technological advancements in general, EFDs in particular. To this effect, future researchers can use the study findings as a reference material. Bearing in mind the fact that the study is theoretical, future researchers may also build on the findings by employing empirical studies where statistics can be used to test the present findings thereby buttressing them numerically.

The novelty of the present study lies on the consolidation, and development of a framework that integrates the benefits of EFDs in the management of taxes through synthesis of fragmented contexts.

7. Limitations

The current study draws its findings from a restricted number of relevant papers that were retrieved. As such, the review cannot be regarded as an exhaustive analysis of the literature on the subject matter. Authors of this paper cannot fully rule out the chances of missing other significant articles in the process of retrieving the analyzed papers especially in light of the fact that most of the analyzed papers were accessed through institutional subscriptions. Furthermore, the selection of keywords utilized to search for the materials is arbitrary and may have resulted in leaving out some relevant papers that could have formed part of the synthesis.

8. Further Research Recommendations

Future researchers may consider retrieving study papers from various main databases (i.e. Scopus, EBSCO, and WoS) with an aim of widening the coverage. Further, quantitative primary study is required where statistics can be tested. Furthermore, focus can be put on establishing the hiccups which tax payers are facing by using EFDs with an aim of coming up with tailor-made solutions to mitigate such challenges and enhance the adoption and utilization of this innovation in the management of taxes. Such hiccups can be established using methodologies like interviews where more insights can be acquired from participants by asking them open ended questions. This will ensure that the innovation is indeed taking into account the needs of both parties.

9. Conclusion

The purpose of this study was to consolidate the benefits of EFDs as recent innovations in the administration of taxes globally. The study used a literature review technique to synthesize extant papers on the subject where four benefits of EFDs as a technical breakthrough in tax administration have been established. Firstly, EFDs minimize tax data manipulation which is rampant when manual collection of taxes is utilized. Secondly, EFDs facilitate real-time transactions by sending tax data to tax administrators instantly thereby increasing efficiency as everything is done promptly. Thirdly, EFDs minimize tax evasion which is common when the traditional methods of collecting taxes have been used thereby boosting revenue collection. Lastly, EFDs offer tax audit trail from the information sources thereby improving tax adherence. In summary, the integration of tax technology in general, EFDs in particular, is essential for efficient tax management as it reduces the difficulties experienced by tax collection agencies during manual tax collection. Adoption of this technology by tax administrators can therefore not be overemphasized as failure to do so leads to losses in revenue collection.

Abbreviations

EDMs

Electronic Device Machines

EFDs

Electronic Funds Devices

TAM

Technology Acceptance Model

TRA

Theory of Reasoned Action

Conflicts of Interest

The authors declare no conflicts of interest.

References

[1]

Abah, J. (2015). Technological innovation and banking in Ghana: An evaluation of customers' perspective. American Academy of Financial Management, 1(3), 338-356.

[2]

Adegbie, F. F. Enerson, J. & Olaoye, S. A. (2022). An empirical investigation into the relationship between electronic tax management system and tax revenue collection efficiency in selected states in South West, Nigeria. International Journal of Accounting Research, 7(1), 43-53.

[3]

Aduamoah, M. Yinghua, S. & Anomah, S. (2017). Applicability of Computerised Accounting System in Improving Financial Accuracy in Ghana SMEs. Innovation and Management.

[4]

Ajayi, E. O. & Yidiat, O. (2021). Impact of e-tax filing on tax revenue generation in Nigeria. Global Journal of Accounting, 7(1), 25-36.

[5]

Almuraqab, N. A. S. & Jasimuddin, S. M. (2017). Factors that Influence End?Users’ Adoption of Smart Government Services in the UAE: A Conceptual Framework. Electronic Journal of Information Systems Evaluation, 20(1), 11-23.

[6]

Allingham, M. & Sandmo, A. (2002). Income tax evasion: A theoretical analysis. Taxation: Critical Perspectives on the World Economy, 3, 305-318.

[7]

Awai, E. S. & Oboh, T. (2020). Ease of paying taxes: The electronic tax system in Nigeria. Accounting and taxation review, 4(1), 63-73.

Flick, U. (2015). Introducing research methodology: A beginner's guide to doing a research project. Sage.

[10]

Islahı, A. (2015). Ibn Khaldun’s theory of taxation and its relevance. Turkish Journal of Islamic Economics, 2(2), 1-19.

[11]

Le, T. N. T. Hai, Y. M. T. Thi, T. C. & Hong, M. N. T. (2024). The Impact of Tax Awareness on Tax Compliance: Evidence from Vietnam. Journal of Tax Reform, 10(2), 214-227.

[12]

Martin, L. O. Obongo, B. M., Magutu, P. O. and Onsongo, C. O (2010). The Effectiveness of Electronic Tax Registers in Processing of Value Added Tax Returns, African [J]. Journal of Business and Management, (1): 44-55.

[13]

Nanthuru, S. B. Pingfeng, L. & Guihua, N. (2017). An Evaluation of Electronic Fiscal Device Effectiveness on Tax Compliance–A Risk Management Innovation: Case Study of Malawi. Innovation and Management, 714-721.

[14]

Olaoye, C. O. & Atilola, O. O. (2018). Effect of e-tax payment on revenue generation in Nigeria. Journal of Accounting, Business and Finance Research, 4(2), 56-65.

[15]

Panneerselvam, R. (2014). Research methodology. PHI Learning Pvt. Ltd.

[16]

Paré, G. Trudel, M. C. Jaana, M. & Kitsiou, S. (2015). Synthesizing information systems knowledge: A typology of literature reviews. Information & management, 52(2), 183-199.

[17]

Popay, J. Roberts, H. Sowden, A. Petticrew, M. Arai, L. Rodgers, M. & Duffy, S. (2006). Guidance on the conduct of narrative synthesis in systematic reviews. A product from the ESRC methods programme Version, 1(1), b92.

[18]

Rosenbusch, N. Rauch, A. & Bausch, A. (2013). The mediating role of entrepreneurial orientation in the task environment–performance relationship: A meta-analysis. Journal of management, 39(3), 633-659.

[19]

Srinivasan T. N. (1973). Tax evasion: A model. Journal of Public Economics, 2(4): 339–346.

[20]

Umenweke, M. N. &Ifediora, E. S. (2016). The law and practice of electronic taxation in Nigeria: The gains and challenges. NAUJILI. 101-112.

[21]

Venkatesh, V. Morris, M. G. Davis, G. B. & Davis, F. D. (2003). User acceptance of information technology: Toward a unified view. MIS quarterly, 425-478.

[22]

Wu, J. H., & Wang, S. C. (2003). An empirical study of consumers adopting mobile commerce in taiwan: analyzed by structural equation modeling. PACIS 2003 Proceedings, 6.

[23]

Xu, Y. (2010). Reforming value added tax in mainland China: a comparison with the EU. Revenue Law Journal, 20(1).

Juma, H. A., Singh, Y. P., Nyoni, A. M. (2026). Essence of Electronic Tax Systems in the Management of Taxes. Science Journal of Business and Management, 14(1), 11-16. https://doi.org/10.11648/j.sjbm.20261401.12

Juma, H. A.; Singh, Y. P.; Nyoni, A. M. Essence of Electronic Tax Systems in the Management of Taxes. Sci. J. Bus. Manag.2026, 14(1), 11-16. doi: 10.11648/j.sjbm.20261401.12

Juma HA, Singh YP, Nyoni AM. Essence of Electronic Tax Systems in the Management of Taxes. Sci J Bus Manag. 2026;14(1):11-16. doi: 10.11648/j.sjbm.20261401.12

@article{10.11648/j.sjbm.20261401.12,

author = {Haji Ameir Juma and Yogendra Pratap Singh and Austin Milward Nyoni},

title = {Essence of Electronic Tax Systems in the Management of Taxes},

journal = {Science Journal of Business and Management},

volume = {14},

number = {1},

pages = {11-16},

doi = {10.11648/j.sjbm.20261401.12},

url = {https://doi.org/10.11648/j.sjbm.20261401.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.sjbm.20261401.12},

abstract = {The deployment of technological innovations to enhance efficiency and accuracy has led to a considerable impact on various commercial sectors globally. In the absence of relevant technological innovations, it would have been burdensome to capture, let alone store and process voluminous commercial transactions. The present paper aims to expounding the significance of electronic device machines (EDMs) as a technological innovation in the management of taxes. A review methodology was utilized to analyze extant literature with regards to the topic. A predetermined inclusion and exclusion criteria was employed to determine the relevance of papers that were analyzed. Through thorough synthesis of articles that were analyzed, the study found four benefits of EDMs as a technological innovation in the management of taxes. Firstly, EDMs prevent tax data manipulation which is rampant when taxes are collected manually; secondly, EDMs allow for real-time transactions where tax data is instantly sent to tax collecting bodies thereby improving efficiency; thirdly, EDMs prevent tax evasion thereby enhancing revenue collection; and finally, EDMs provide tax audit trail from the data sources thereby enhancing tax compliance. In a nutshell, adoption of EDMs as a technological innovation is vital in the process of managing tax as it minimizes challenges faced by tax collecting bodies when the exercise is done manually.},

year = {2026}

}

TY - JOUR

T1 - Essence of Electronic Tax Systems in the Management of Taxes

AU - Haji Ameir Juma

AU - Yogendra Pratap Singh

AU - Austin Milward Nyoni

Y1 - 2026/01/30

PY - 2026

N1 - https://doi.org/10.11648/j.sjbm.20261401.12

DO - 10.11648/j.sjbm.20261401.12

T2 - Science Journal of Business and Management

JF - Science Journal of Business and Management

JO - Science Journal of Business and Management

SP - 11

EP - 16

PB - Science Publishing Group

SN - 2331-0634

UR - https://doi.org/10.11648/j.sjbm.20261401.12

AB - The deployment of technological innovations to enhance efficiency and accuracy has led to a considerable impact on various commercial sectors globally. In the absence of relevant technological innovations, it would have been burdensome to capture, let alone store and process voluminous commercial transactions. The present paper aims to expounding the significance of electronic device machines (EDMs) as a technological innovation in the management of taxes. A review methodology was utilized to analyze extant literature with regards to the topic. A predetermined inclusion and exclusion criteria was employed to determine the relevance of papers that were analyzed. Through thorough synthesis of articles that were analyzed, the study found four benefits of EDMs as a technological innovation in the management of taxes. Firstly, EDMs prevent tax data manipulation which is rampant when taxes are collected manually; secondly, EDMs allow for real-time transactions where tax data is instantly sent to tax collecting bodies thereby improving efficiency; thirdly, EDMs prevent tax evasion thereby enhancing revenue collection; and finally, EDMs provide tax audit trail from the data sources thereby enhancing tax compliance. In a nutshell, adoption of EDMs as a technological innovation is vital in the process of managing tax as it minimizes challenges faced by tax collecting bodies when the exercise is done manually.

VL - 14

IS - 1

ER -

Juma, H. A., Singh, Y. P., Nyoni, A. M. (2026). Essence of Electronic Tax Systems in the Management of Taxes. Science Journal of Business and Management, 14(1), 11-16. https://doi.org/10.11648/j.sjbm.20261401.12

Juma, H. A.; Singh, Y. P.; Nyoni, A. M. Essence of Electronic Tax Systems in the Management of Taxes. Sci. J. Bus. Manag.2026, 14(1), 11-16. doi: 10.11648/j.sjbm.20261401.12

Juma HA, Singh YP, Nyoni AM. Essence of Electronic Tax Systems in the Management of Taxes. Sci J Bus Manag. 2026;14(1):11-16. doi: 10.11648/j.sjbm.20261401.12

@article{10.11648/j.sjbm.20261401.12,

author = {Haji Ameir Juma and Yogendra Pratap Singh and Austin Milward Nyoni},

title = {Essence of Electronic Tax Systems in the Management of Taxes},

journal = {Science Journal of Business and Management},

volume = {14},

number = {1},

pages = {11-16},

doi = {10.11648/j.sjbm.20261401.12},

url = {https://doi.org/10.11648/j.sjbm.20261401.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.sjbm.20261401.12},

abstract = {The deployment of technological innovations to enhance efficiency and accuracy has led to a considerable impact on various commercial sectors globally. In the absence of relevant technological innovations, it would have been burdensome to capture, let alone store and process voluminous commercial transactions. The present paper aims to expounding the significance of electronic device machines (EDMs) as a technological innovation in the management of taxes. A review methodology was utilized to analyze extant literature with regards to the topic. A predetermined inclusion and exclusion criteria was employed to determine the relevance of papers that were analyzed. Through thorough synthesis of articles that were analyzed, the study found four benefits of EDMs as a technological innovation in the management of taxes. Firstly, EDMs prevent tax data manipulation which is rampant when taxes are collected manually; secondly, EDMs allow for real-time transactions where tax data is instantly sent to tax collecting bodies thereby improving efficiency; thirdly, EDMs prevent tax evasion thereby enhancing revenue collection; and finally, EDMs provide tax audit trail from the data sources thereby enhancing tax compliance. In a nutshell, adoption of EDMs as a technological innovation is vital in the process of managing tax as it minimizes challenges faced by tax collecting bodies when the exercise is done manually.},

year = {2026}

}

TY - JOUR

T1 - Essence of Electronic Tax Systems in the Management of Taxes

AU - Haji Ameir Juma

AU - Yogendra Pratap Singh

AU - Austin Milward Nyoni

Y1 - 2026/01/30

PY - 2026

N1 - https://doi.org/10.11648/j.sjbm.20261401.12

DO - 10.11648/j.sjbm.20261401.12

T2 - Science Journal of Business and Management

JF - Science Journal of Business and Management

JO - Science Journal of Business and Management

SP - 11

EP - 16

PB - Science Publishing Group

SN - 2331-0634

UR - https://doi.org/10.11648/j.sjbm.20261401.12

AB - The deployment of technological innovations to enhance efficiency and accuracy has led to a considerable impact on various commercial sectors globally. In the absence of relevant technological innovations, it would have been burdensome to capture, let alone store and process voluminous commercial transactions. The present paper aims to expounding the significance of electronic device machines (EDMs) as a technological innovation in the management of taxes. A review methodology was utilized to analyze extant literature with regards to the topic. A predetermined inclusion and exclusion criteria was employed to determine the relevance of papers that were analyzed. Through thorough synthesis of articles that were analyzed, the study found four benefits of EDMs as a technological innovation in the management of taxes. Firstly, EDMs prevent tax data manipulation which is rampant when taxes are collected manually; secondly, EDMs allow for real-time transactions where tax data is instantly sent to tax collecting bodies thereby improving efficiency; thirdly, EDMs prevent tax evasion thereby enhancing revenue collection; and finally, EDMs provide tax audit trail from the data sources thereby enhancing tax compliance. In a nutshell, adoption of EDMs as a technological innovation is vital in the process of managing tax as it minimizes challenges faced by tax collecting bodies when the exercise is done manually.

VL - 14

IS - 1

ER -